TV advertising at 70: Viewing habits, ad spend and effectiveness

As ITV marks 70 years of TV advertising, shifting definitions of what counts as ‘TV’, changing viewing habits and evolving levels of ad spend are reshaping the medium.

On this day 70 years ago, the first ad – one for Gibbs SR toothpaste – aired on British TV for the first time as ITV launched.

On this day 70 years ago, the first ad – one for Gibbs SR toothpaste – aired on British TV for the first time as ITV launched.

Even back then, TV was hailed as effective. The man behind Britain’s first TV ad, Brian Palmer told the BBC in 2015 that despite “not many people” having a TV in 1955, the ad “did have a favourable effect on sales”.

Since that first broadcast, both the UK advertising landscape and the way audiences consume content have changed dramatically.

Marketers now navigate a growing web of screens, platforms and acronyms – BVOD, SVOD, AVOD, FAST, CTV – each representing a new path to reach viewers.

More recently, the very definition of “TV” is under debate: is it determined by format, device or media owner?

The state of TV viewing

Online platforms and devices have reshaped viewing habits and advertising models. In 2025, British adults are spending more time on mobile phones than in front of traditional TV sets for the first time, according to IPA data.

Meanwhile, there is a departure from linear TV. In 2024, 73.8% of individuals watched broadcast TV each week on TV sets, according to Ofcom.

Although this was a 1.7 percentage point year-on-year decrease, it was less than the 3.8 percentage point drop between 2022 and 2023. Weekly reach was highest among those aged 65-plus (94%) and lowest among 16 to 24s (45%). By comparison, this figure stood at 93.4% in 2005 and 93.5% in 2015, according to BARB.

‘The audience is harder to find’: How brands’ AV strategies are evolving

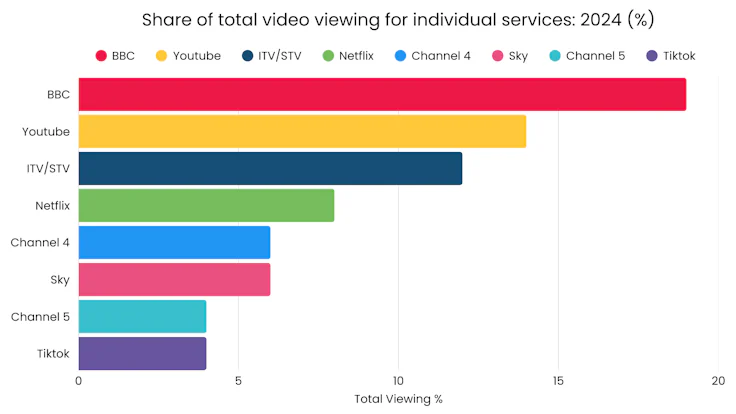

Comparatively, YouTube is emerging as the top destination for younger viewers, changing how Brits watch television. Ofcom reports that 20% of Gen Alpha (aged four to 15) head straight to the YouTube app as soon as they turn the TV on. It was second only to the BBC as a media destination.

It’s not solely younger people. Over-55s are now watching twice the amount of YouTube content on their TVs than they were last year (11 minutes per day compared to six minutes per day in 2023) and 42% of all YouTube viewing by this age group is on a TV set.

YouTube, for its part, is quickly becoming more of a traditional viewing platform in its own right. Ofcom’s research shows half of the platform’s top trending videos now more closely resemble traditional TV.

However, the jury is still out on whether YouTube can be considered TV. Unlike traditional broadcasters such as ITV, Channel 4, or even subscription services like Netflix, YouTube is not subject to the same regulatory framework. This raises a broader question: does TV refer to a specific ad format, a type of media owner, or simply the largest screen in the home?

To reflect changing viewing habits, the Advertising Association and Warc recently expanded their definition of total TV.

The updated definition now includes broadcaster video-on-demand (BVOD), ad-supported subscription video-on-demand (SVOD) such as Disney+, Netflix, and Prime Video, advertising-based video-on-demand (AVOD), and free ad-supported streaming TV (FAST). Notably, YouTube is excluded.

Meanwhile, Thinkbox defines TV as “high quality, professionally produced and commissioned”.

“It is strictly regulated and measured. It can be watched live or on-demand on any screen but is predominantly watched on TVs. It can be watched via TV channels, TV apps, or multi-form video platforms like YouTube. It is a medium any genre can burst to life in,” explains Thinkbox CEO Lindsey Clay.

Last week, the UK’s public service broadcasters (PSB) issued a joint letter warning that without government action, they risk being overtaken by global online platforms “driven by profit, not purpose”.

Writing ahead of the Royal Television Society’s Cambridge Convention, the BBC, ITV, Channel 4, Channel 5, STV, S4C and MG ALBA called for five key measures: ensuring PSB content and impartial news are prominent on all platforms, boosting investment in UK storytelling through tax credits and sustainable funding, setting a date for a national switchover to internet-delivered TV in the 2030s and removing barriers to strategic partnerships.

How TV is defined impacts how advertisers allocate budgets. “Gone are the days when you would do a TV buy, with 70% of the budget on TV, and then 30% on YouTube,” Carwow’s CMO Ben Carter told Marketing Week earlier this year.

Shifting investment patterns

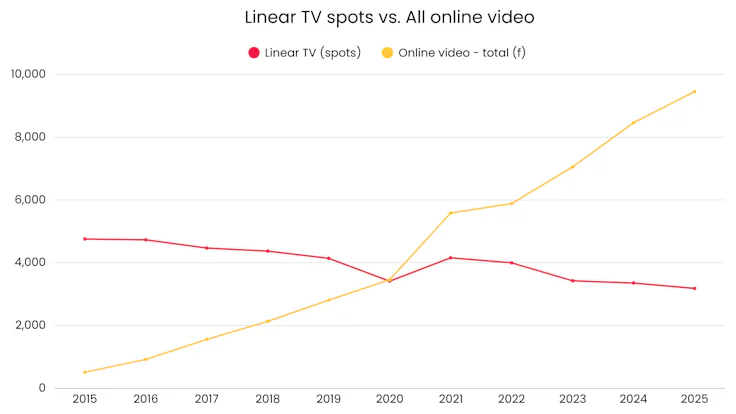

As linear TV viewing declines, audiences are migrating to connected TV (CTV) platforms, and advertising investment is following.

Since 2015, linear TV ad spend has dropped by an average of 33.1% year-on-year, according to figures from Warc. In contrast, total online video – including BVOD, SVOD, social media and open web video – has grown 1,759.4% over the same period, demonstrating that digital investment is increasingly significant, even for traditional broadcasters.

Yet the narrative of linear decline overlooks the fact that TV has always evolved. After a brief contraction, UK TV advertising returned to growth in 2024, with total spend reaching £5.27bn, a 3.8% increase year-on-year, according to AA and Warc.

Primark, for instance, aired its first-ever TV ad earlier this month despite 50 years on the high street.

“TV brings that brand, emotive element that you can’t always get through performance marketing and especially when you’re trying to make somebody think a little bit differently or to reconsider the brand. It felt like the right time to do it,” says Primark’s marketing director, Wendy Duggan.

And ground is being made up for broadcasters who are investing in digital: “The growth in our digital revenue has largely offset the decline in linear,” ITV’s CEO Dame Carolyn McCall declared on the broadcaster’s 2024 full-year earnings call.

Clay suggests there’s an “odd, slightly blinkered focus” on linear TV viewing, which is like “judging the popularity of the Tube based solely on use of the Central Line”.

“Linear is still huge, but TV is much more than that now – and younger viewers in particular lean towards streaming and on demand TV – and they probably watch some of the TV that’s on YouTube. Their TV journeys are different, but they’re still on board,” she adds.

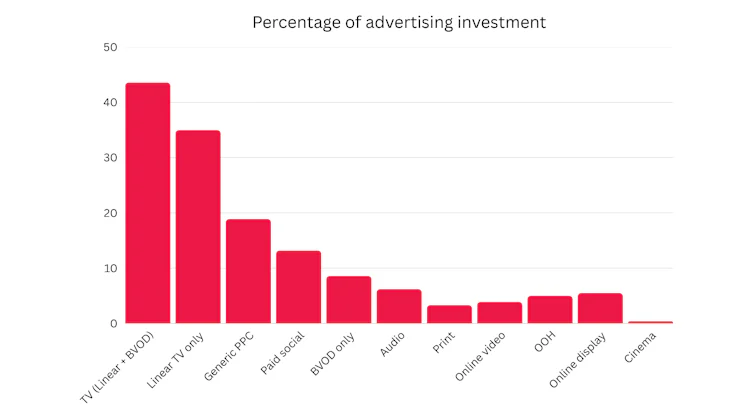

When total TV, which now includes the likes of Netflix, Amazon Prime and similar platforms, is compared with wider online video, the picture appears more balanced.

Removing social media from the comparison changes the picture. When total TV is measured against online video that excludes both social media and TV, investment in online video – mainly open web video – is far smaller than total TV spend.

Because YouTube is classified as social media, the data also shows that much of the growth in ad spend is flowing to social platforms rather than other online video and total TV remains strong.

Therefore, most advertisers are currently thinking about AV campaigns more broadly and view TV as one component of a broader strategy that also comprises video on demand and sharing platforms.

Mobile network Three is one brand asking exactly that. Five years ago, it shifted away from a youth-first strategy, expanding its target to the entire UK population. To do so, it moved around two-thirds of its budget from social media into broader-reach channels like linear TV, a strategy it claims has worked.

Since making that shift, however, Chris Gough, head of marketing and communications at Three UK, says there’s been “big changes” in the landscape, and the challenge now is to focus on how to build on its reach.

“What we’ve seen since 2020 is that we get the same reach on linear TV now as in 2020, but it costs about two and a half times as much,” explains Gough.

As a result, Three is rebalancing again. this time toward SVOD and CTV, while staying “cognisant” of where the brand appears.

“What we don’t want is to do this dramatic shift where suddenly you’re going from a plan that is linear TV, which is quality content, to a load of programmatic stuff, and you’re next to a load of cat videos,” he explains.

Ad-funded SVOD triples weekly reach as smartphone viewing overtakes TV

Meanwhile, growth in subscription video-on-demand (SVOD) services like Netflix, Amazon Prime, and Disney+ has plateaued in recent years, but the sector is now entering the early stages of advertising.

Ad-funded subscriptions have nearly tripled their weekly reach in the UK over the past year, creating new opportunities for advertisers.

According to IPA data, SVOD services now reach 30% of adults weekly, up from 11% in 2024 and 10% in 2023. Netflix leads with a 16% weekly reach, followed by Amazon Prime (15%) and Disney+ (7%).

Advertisers are clearly paying attention. Investment in SVOD, AVOD, and FAST platforms was £236m in 2024, more than double 2023’s £96m, per AA/Warc figures.

Is TV still effective?

Falling TV audiences do not necessarily mean falling effectiveness. Broadcast TV continues to be one of the most trusted advertising environments, and evidence suggests it still delivers significant brand impact.

A major 2024 study, Profit Ability 2, commissioned by Thinkbox and independently analysed using £1.8bn of UK media investment across 10 channels, 141 brands and 14 categories, found TV remains the most profitable medium.

TV accounts for 54.7% of total advertising-generated profit, with an average ROI of £5.61 for every £1 spent. Of that, linear TV accounted for 46.6% of payback and BVOD 8.2%.

The study also found that TV has the highest saturation point – the last point where every pound invested in a channel generates at least £1 profit at £330,000. Advertisers can increase their investment in TV to a higher level than other media and it will continue to generate a profitable return.

GroupM expanded on this analysis with simulations of 7,488 brand examples and 52,416 scenarios, comparing the impact of removing TV entirely versus proportionate cuts across all channels.

Removing TV could reduce campaign profits by 24% within three months and 60% over two years. On a national scale, the UK advertising industry could forfeit nearly £28bn in profit if TV were completely removed from media plans.

The future of TV

Broadcasters are increasingly looking beyond traditional spots and sponsorships to diversify their revenue. Alternative streams such as product placement, branded content and advertiser-funded programming remain relatively small, but are becoming an important growth area.

Channel 4 has expanded its branded-content output, enabling brands to co-create TV-style content for both broadcast and social platforms. ITV is doing the same by relaunching its branded entertainment arm as BE Studio, set up to partner with advertisers on similar projects.

‘A leap of faith’: Three brands on the value of ad-funded programming

At the same time, broadcasters are working to make TV advertising more accessible to smaller and medium-sized brands. ITV and Channel 4 have both introduced generative AI ad tools designed to lower production costs and simplify the media-buying process.

ITV has just launched a suite of new ad tools, including dynamic pause ads, with custom adverts generated for users on ITVX when they pause on-demand content on connected TVs.

Meanwhile, the quest for more accurate and wide-ranging measurement is ongoing.

ITV, Sky and Channel 4 have been hoping to provide advertisers with a means of quantifying TV’s effect on short-term performance metrics to help “pave a way for a more transparent approach to advertising effectiveness”.

The three broadcasters are working on a joint measurement tool, Lantern, to “give [TV] the measurement it deserves”. If progress continues as planned, Lantern will be operating at full scale in 2026.